meganwoolsey Home

meganwoolsey Home

Related Articles

Super Micro Computer (NASDAQ: SMCI) investors have been on a roller-coaster ride in 2024. The stock entered the year at $280, then it quickly peaked at nearly $1,200 in March. Since then, it’s been a near-straight fall down, and the stock currently sits around $440.

There are some good reasons why Supermicro fell from its $1,000-plus stock price earlier this year, but I also think its current price is an absolute steal, which is why I just bought the dip on the stock.

Supermicro hasn’t had much positive news lately

Super Micro Computer builds components for computing servers as well as full server solutions themselves. Its claim to fame in this world is that it offers highly customizable servers that can be tailored for any workload size or type. Additionally, its liquid-cooled technology alongside other innovations make its servers the most efficient in the world. This is critical, as the energy input costs into these servers are incredibly high.

With massive demand for data center parts and servers, Supermicro’s business has boomed, following a similar growth trajectory as Nvidia. This caused the stock to rise earlier this year, but the company has hit two major stumbling blocks along the way.

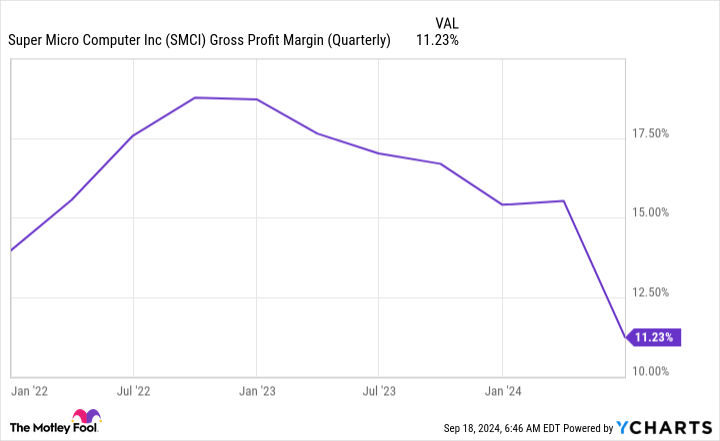

First, Supermicro’s gross margin plummeted in 2024, continuing a trend that started in 2023.

This is a problem, as a plummeting gross margin can signal pricing competition, indicating that Supermicro has no real competitive advantages. However, management points to the upfront costs of getting its liquid cooling technology up and running. It expects its gross margin to improve as components become more readily available throughout fiscal year 2025 (ending June 2025).

This should also improve bottom-line profitability and is a key trend to watch over the next year.

The second cause for Supermciro’s decline was Hindenburg Research’s short report. Hindenburg is a famed short-seller, which means it profits as the stock declines. It is known to release reports on various companies, explaining why it believes the stock is mispriced. In Supermicro’s case, it alleges accounting malpractice as one of the chief concerns. Supermicro didn’t do itself any favors in beating these allegations by delaying its end-of-year form 10K filing to the Securities and Exchange Commission (SEC) either.

The Hindenburg report doesn’t concern me as much as the falling margins do, as if there are any issues, it likely only accounts for a very small fraction of Supermicro’s business.

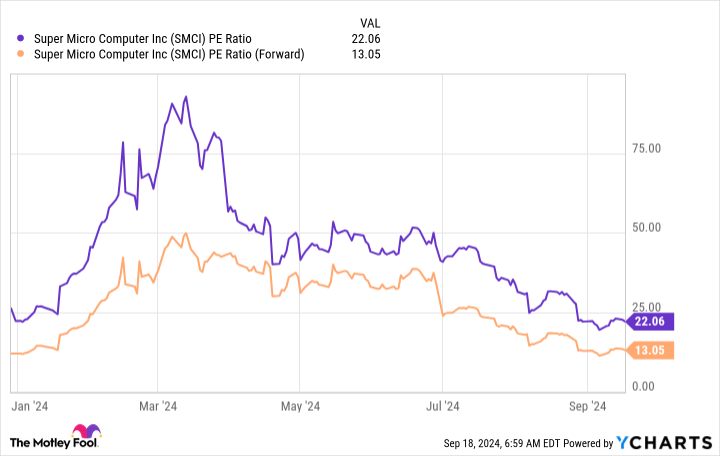

As for the margins, the market is valuing the stock like it will never return to normal, which is a huge investment opportunity.

The bar is fairly low for Supermicro’s stock to succeed

Fiscal year 2025 is expected to be another monster year of growth for Supermicro, with revenue expected to rise between 74% and 101% year over year. Furthermore, Supermicro’s CEO raised his long-term outlook to $50 billion in annual revenue for the company. There’s a massive opportunity here, and Supermicro will be one of the primary beneficiaries.

According to Wall Street estimates, Supermicro is projected to grow its earnings by 69% in fiscal 2025.

However, if Supermicro meets its revenue growth targets, its revenue growth will exceed earnings growth projections. This doesn’t make much sense, especially if margins improve throughout the year, as management forecasts.

This is a key reason why I’m investing in Supermicro: The stock’s base case is easily achievable. If Supermicro knocks it out of the park, grows revenue at the high end of expectations, and improves margins, the stock will likely be a home run.

With the general trends toward cloud computing and artificial intelligence (AI), Supermicro’s business isn’t slowing down anytime soon. As a result, I’m using the weakness to start a position, as it could be a huge winner in the next few years.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $722,320!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 16, 2024

Keithen Drury has positions in Super Micro Computer. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

I Just Bought the Dip on Super Micro Computer Stock was originally published by The Motley Fool

Source link