meganwoolsey Home

meganwoolsey Home

Related Articles

It’s no secret that semiconductor stocks have been particularly big winners amid the artificial intelligence (AI) revolution. With share prices skyrocketing, several high-profile chip companies have opted for stock splits this year. Some AI chip stock-split stocks you might recognize include Nvidia (NASDAQ: NVDA), Super Micro Computer (NASDAQ: SMCI), and Broadcom (NASDAQ: AVGO).

Indeed, each of these stocks has done wonders for many portfolios over the last couple of years. However, I see one of these chip stocks as the superior choice over its peers.

Let’s break down the full picture at Nvidia, Supermicro, and Broadcom and determine which AI chip stock-split stock could be the best buy-and-hold opportunity for long-term investors.

1. Nvidia

For the last two years, Nvidia has not only been the biggest name in the chip space but also essentially emerged as the ultimate gauge of AI demand at large. The company specializes in designing sophisticated chips, known as graphics processing units (GPUs), and data center services. Moreover, Nvidia’s compute unified device architecture (CUDA) provides a software component that can used in conjunction with its GPUs, providing the company with an enviable and lucrative end-to-end AI ecosystem.

While all that looks great, investors cannot afford to be starry-eyed due to Nvidia’s existing dominance. The table below breaks down Nvidia’s revenue and free-cash-flow growth trends over the last several quarters.

|

Category |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

Q2 2024 |

|---|---|---|---|---|---|

|

Revenue |

101% |

206% |

265% |

262% |

122% |

|

Free cash flow |

634% |

Not material |

553% |

473% |

125% |

Data source: Nvidia Investor Relations.

Admittedly, it’s hard to throw shade on a company that is consistently delivering triple-digit revenue and profit growth. My concern with Nvidia is not related to the level of its growth but rather its pace.

For the company’s second quarter of fiscal 2025 (ended July 28), Nvidia’s revenue and free cash flow rose 122% and 125% year over year, respectively. This is a notable slowdown from the last several quarters. It’s fair to point out that the semiconductor industry is cyclical, and a factor like that could influence growth in any given quarter. Unfortunately, I think there’s more beneath the surface with Nvidia.

Namely, Nvidia faces rising competition from direct industry forces, such as Advanced Micro Devices, and tangential threats from its customers — namely, Tesla, Meta, and Amazon. In theory, as competition in the chip space rises, customers will have more options.

This leaves Nvidia with less leverage, which will likely diminish some of its pricing power. In the long run, this could take a hefty toll on Nvidia’s revenue and profit growth. For these reasons, investors might want to consider some alternatives to Nvidia.

2. Super Micro Computer

Supermicro is an IT architecture company specializing in designing server racks and other infrastructure for data centers. In recent years, soaring demand for semiconductor chips and data center services has served as a bellwether for Supermicro. Moreover, the company’s close alliance with Nvidia has proved particularly beneficial.

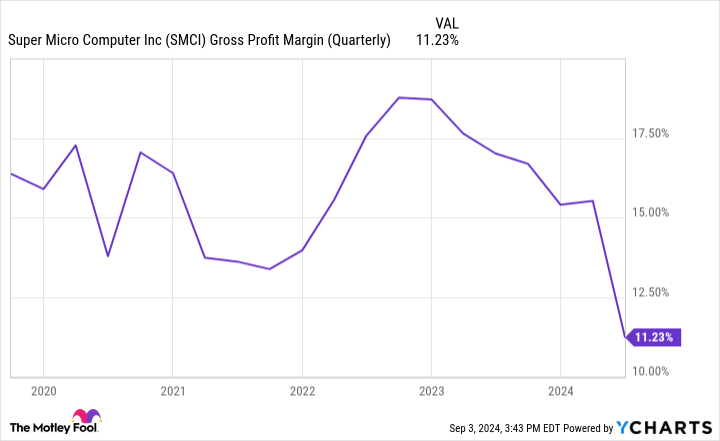

That said, I have some concerns with Supermicro. As an infrastructure business, the company relies heavily on other companies’ capital expenditure needs. This makes Supermicro’s growth susceptible to external variables, such as demand for data center services, chips, server racks, and more. Furthermore, Supermicro is far from the only IT architecture specialist in the market.

Competition from Dell, Hewlett Packard, and Lenovo (just to name a few) bring their own levels of expertise to the marketplace. As a result of competing in such a commoditized atmosphere, Supermicro can be forced to compete on price — which takes a toll on profit generation.

Infrastructure businesses do not carry the same margin profile as software companies, for instance. Given that the company’s gross margins are fairly low and in decline, investors must be cautious. While Supermicro’s management tried to assure investors that the margin deterioration is the result of some logjams in the supply chain, more recent news might signal that gross margin is the least of the company’s concerns.

Supermicro was recently the target of a short report published by Hindenburg Research. Hindenburg alleges that Supermicro’s accounting practices have some flaws. Following the short report, Supermicro responded in a press release outlining that the company is delaying its annual filing for fiscal year 2024.

Given the unpredictability of demand prospects, a fluctuating margin and profit dynamic, and the allegations surrounding its accounting practices, I think investors now have better options in the chip space.

3. Broadcom

By process of elimination, it’s clear that Broadcom is my top buy-and-hold choice among chip stocks right now. This is not because Broadcom’s returns this year have lagged its counterparts, though. The underlying reasons Broadcom’s shares have paled compared to other chip stocks could shine some light on why I think its best days are ahead.

I see Broadcom as a more diversified business than Nvidia and Supermicro. The company operates across a host of growth markets, including semiconductors and infrastructure software. Grand View Research estimates that the total addressable market for systems infrastructure in the U.S. was valued at $136 billion back in 2021 and was set to grow at a compound annual growth rate of 8.4% between 2022 and 2030.

Systems infrastructure comprises opportunities in data centers, communications, cloud computing, and more. Considering corporations of all sizes are increasingly relying on digital infrastructure to make data-driven decisions, I see the role Broadcom plays in network security and connectivity as a major opportunity and think its recent acquisition of VMware is particularly savvy and will help unlock new growth potential.

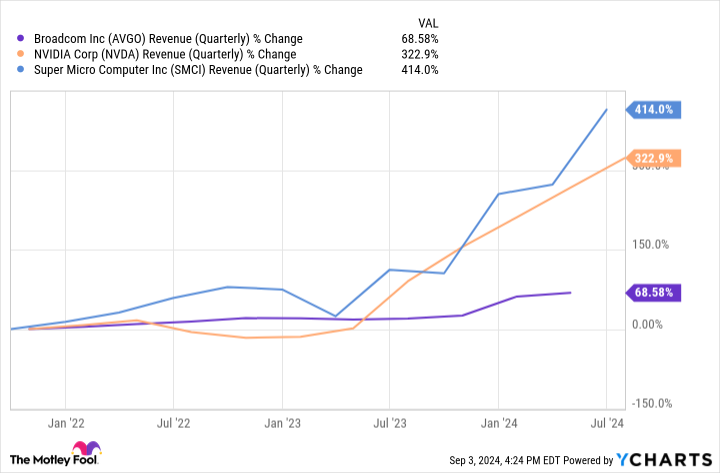

If you look at the growth trends in the chart above, it’s obvious that Broadcom is not experiencing the same level of demand as Nvidia and Supermicro right now. I think this is because Broadcom’s position in the broader AI realm is yet to experience commensurate growth compared to buying chips and storage solutions in droves.

While I’m not saying Nvidia or Supermicro are poor choices, I think their futures look cloudier than Broadcom’s right now. I believe Broadcom is in the very early stages of a new growth frontier featuring many different themes (with AI being just one of them). For these reasons, I see Broadcom as the best option explored in this piece and think long-term investors have a lucrative opportunity to scoop up shares and hold on tight.

Should you invest $1,000 in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $630,099!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 3, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Amazon, Meta Platforms, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Meta Platforms, Nvidia, and Tesla. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Nvidia, Super Micro, or Broadcom? Meet the Artificial Intelligence (AI) Stock-Split Stock I Think Is the Best Buy and Hold Over the Next 10 Years. was originally published by The Motley Fool

Source link